China's IC industry development faces three major opportunities

China's IC industry development faces three major opportunities:

1. Since 2010, global semiconductor sales and investment have entered a new round of high growth;

2. The dependence of China's IC industry on foreign countries is still strong, and the demand for localization is urgent;

3. The State established a large fund to focus on the IC industry. At the current time, it is recommended that all types of capital increase investment in the integrated circuit industry. Through the combination of industry and finance, promote the coordinated development of all links in the industrial chain, and form a supporting system for the upstream and downstream Jackie Chan, thus realizing the leap-forward development of the integrated circuit industry.

I. Development of China's integrated circuits in 2017

1.1 Global and Chinese market sales increased by more than 20%

In 2017, global semiconductor sales are expected to reach US$408.7 billion, up 20.6% year-on-year. Among them, the integrated circuit industry is 340.2 billion US dollars, and the increase in memory prices is the largest.

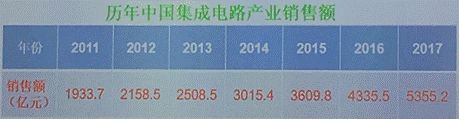

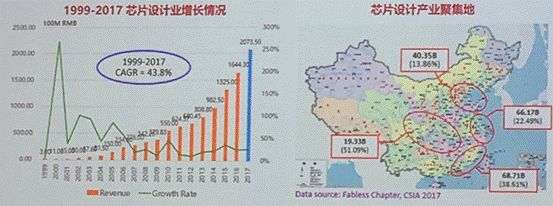

In 2017, the sales of China's IC industry was 535.52 billion yuan, a year-on-year increase of 23.5%. The design, manufacturing, packaging and testing increased by 24.7%/29.1%/18.3%, respectively, accounting for 38.3%/27.2%/34.5%. .

1.2 China's integrated circuit import and export situation: The external dependence of the IC industry is still strong, and the import and export deficit is still huge.

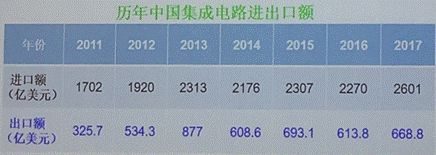

According to statistics, in 2017, the import value of China's integrated circuits reached 260.14 billion US dollars, an increase of 14.6%, the export value was 66.88 billion US dollars, and the import and export deficit was 193.26 billion US dollars, an increase of 16.6%. As can be seen from the data, the demand for localization of Chinese integrated circuits is very urgent.

Second, China's development of integrated circuit industry opportunities

2.1 High-level policy guidance:

Report of the 19th National Congress: Proposing to build a network power, digital China, and a smart society;

The government work report of 2018: The integrated circuit ranks first in the real economy, which shows that the government supports the integrated circuit. In 2018, the integrated circuit has entered a new journey of the real economy.

The work conference of the Ministry of Industry and Information Technology in 2018: proposed to implement the "Made in China 2025" in depth; promote the construction of a network powerhouse; promote the deep integration of the Internet, big data, artificial intelligence and manufacturing, develop and expand the digital economy; accelerate the optimization and upgrading of the traditional economy.

2.2 The local level also regards integrated circuits as a strategic pillar industry to develop

Beijing, Shanghai, Shenzhen, Jiangsu, Hubei, Wuhan and other foundations are relatively strong. Now Fujian, Hefei, Chengdu, Xi'an, etc. also attach great importance to the integrated circuit industry, and give strong support in terms of policies, funds and talents.

2.3 China's integrated circuit industry development goals and main tasks (according to the "National Integrated Circuit Industry Development Promotion Outline")

By 2015, the innovation of integrated circuit development system and mechanism has achieved remarkable results, establishing a financing platform and policy environment that is compatible with the law of industrial development, with industrial sales exceeding 350 billion yuan;

By 2020, the gap between the integrated circuit industry and the international advanced level will gradually narrow, and the annual growth rate of sales revenue of the whole industry will exceed 20%;

By 2030, the main links of the IC industry chain have reached the international advanced level, and a number of enterprises have entered the international first echelon.

Current major tasks cover design, manufacturing, advanced packaging testing, key equipment and materials.

2.4 New hotspots and future core products in the semiconductor industry

There are many hot spots in the industry, and they are also concentrated, including cloud computing, Internet of Things, big data, industrial Internet, 5G;

Strategic guidance includes China Manufacturing 2025 (Intelligent Manufacturing), Internet +, Big Data;

Artificial intelligence: The 19th report and the work report of the two sessions put AI in a high position, including robots, drones, new energy vehicles/Intelligent network vehicles, and driverless driving;

In addition to the traditional silicon-based chips we are developing, the latter hotspots may be compound semiconductors (GaN, SiC, etc.); future high-end chips (including CPU, FPGA, AD/DA, MEMS sensors) and other core products.

3. Overview of the development of China's electronic information manufacturing industry in 2017

China's electronics market is the largest in the world, generating a large demand for chips. In 2017, China's above-scale electronic information manufacturing industry achieved sales revenue of 14 trillion yuan, a year-on-year increase of 14%, 7.2 percentage points higher than the growth rate of all industries above designated size.

From the perspective of the main terminal products downstream of the electronic information industry, the output of notebook computers and smart TVs in China has increased by about 7% in 2017.

Fourth, the progress of the National Fund

By the end of 2017, the National Fund had been established for more than three years, investing a total of 49 enterprises, accumulating effective investment in 67 projects, accumulative project commitments of 118.8 billion yuan, and actually investing 81.8 billion yuan, respectively, accounting for the total scale of the first phase. 86% and 61%.

To sum up, cover the entire industrial chain of design, manufacturing, packaging and testing, equipment, materials and ecological construction in the manufacturing sector. Specifically, advanced technologies in the manufacturing field, including SMIC and Qualcomm, focus on Wuhan Yangtze River storage in terms of storage, which is the most important manufacturing part; in terms of design, communication, digital cloud video products, storage control, Non-generic storage products; in terms of assembly, Zhongwei, North Huachuang. We are also very happy to see that the investment target has made a breakthrough in the capital market. In 17 years, two investment companies were listed on the Shenzhen Stock Exchange, one listed on the Hong Kong Stock Exchange and one listed on the Nasdaq. In general, the operation of the capital market It is successful.

V. Summary: Accelerate the integration of industry and finance and accelerate industrial development

Integrated circuits are our strategic industries and pillar industries. China must enlarge and strengthen its own integrated circuit industry. It is recommended that all types of capital increase investment in the integrated circuit industry. Through the combination of industry and finance and long-term efforts, promote the coordinated development of all links in the industrial chain, and form a supporting system for the upstream and downstream Jackie Chan, so as to truly realize the leap-forward development of the integrated circuit industry.

Chapter 2 Detailed data of the global and Chinese integrated circuit market in 2017

Wei Shaojun, Director, Institute of Microelectronics, Tsinghua University

I. The global IC industry has grown substantially in 2017

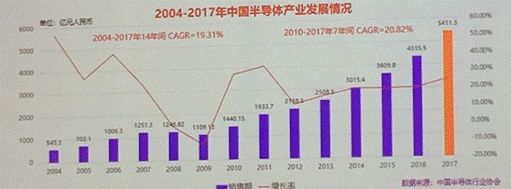

In 2017, the global semiconductor industry sales of 419.7 billion US dollars, an increase of 23.8%, is the fastest growth year since 2011. Unlike the previous year of significant growth in 2010, this significant increase occurred in the absence of significant changes in the market and application equipment, and was marked by a rapid and substantial increase in memory prices.

Second, China's IC industry continues to maintain rapid growth in 2017

In 2017, the annual sales of China's integrated circuits reached 541.1 billion yuan, a year-on-year increase of 24.8%. It is also the fastest since 2012, and the first high growth rate has been rid of the growth rate of around 20% in recent years.

3. Manufacturing, design, packaging and testing of China's IC industry in 2017

In 2017, all major segments of China's IC industry maintained rapid growth, and the growth rates of design, manufacturing and packaging testing exceeded 20%, the first time in recent years. Among them, the chip manufacturing industry has the highest growth rate of 28.5%; the design industry ranks second with 26.1%, and the sales volume has exceeded 200 billion for the first time; the packaging and testing industry whose growth rate has stayed below 20% for a long time has also achieved the best in recent years. Achievements, growth rate also exceeded 20%.

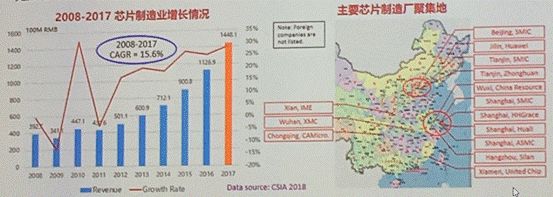

In 2017, the annual sales of China's chip manufacturing industry reached 144.8 billion yuan, an increase of 28.5% over the previous year, the highest value in recent years. However, it must be pointed out that this value includes the operating data of foreign-owned enterprises in China, so the rapid growth of manufacturing includes the contribution of these enterprises.

In 2017, China's chip design sales reached 207.3 billion yuan, surpassing 200 billion for the first time, and unlike chip manufacturing, chip design statistics are almost all local companies, and given the final output of chip design products, with global industry sales statistics The conditions under which the data is compared are therefore of great concern.

Fourth, the import and export of China's integrated circuits in 2017

Since 2013, the value of China's imported integrated circuits has exceeded 200 billion US dollars. This phenomenon reappeared in 2017 and reached a record high. In 2017, the value of integrated circuits was US$260.1 billion, while the import of crude oil in 17 years was US$162.3 billion, far below the value of imported chips. Although there are some factors that increase the price of some integrated circuits, the value of imported chips exceeds 200 billion US dollars. There is no doubt that the resulting trade deficit has reached a record high of 193.2 billion US dollars.

Chapter III Strengthening cooperation with international capital to promote Chinese enterprises to go out

Ye Tianchun, Director of Institute of Microelectronics, Chinese Academy of Sciences

Mr. Ye’s speeches in the past few years have been based on the theory of technology, “talking about industry=â€, and this kind of transformation is also a portrayal of the development path of China’s integrated circuit industry.

In the past ten years, we can see from the special project 02 that China has been committed to the cultivation of the semiconductor industry, including the construction of equipment, materials, manufacturing processes and other industrial chains. We found that in the process of gradual growth, Zhongwei Semiconductor, North Microelectronics, and Jiangfeng Electronics, on the one hand, must develop technology, do research and development, and market, and carry out upstream and downstream integration. On the other hand, investment and financing are indispensable. . Therefore, in the special project of 02, we proposed that the development of the IC industry requires the combination of the industrial chain, the innovation chain, and the financial chain. A few years ago, we first proposed to the State Council the idea of ​​establishing an industrial investment fund, and the National Fund, which was established later, has Great results have been achieved.

However, from our point of view, there are not enough funds, and even local government funds are not enough. From angels, early and middle VCs, to PE, industry integration, especially in the early and early VCs that have been fostered for a long time, China has just Start. We have found that a large amount of capital enters the industry, but these funds are often blind. I don't know about the future development of the industry and the way to cultivate it. Even we found that many projects that should be eliminated, in the third- and fourth-tier cities, combined with local governments and real estate, have come back to life. Investors need to have the ability and experience to choose projects, guide development, and go all the way.

The second is to strengthen the integration of domestic and international capital. International capital M&A funds are many billions of dollars in size and are more professional and forward-looking. And now many investment projects are Chinese projects, and there are few overseas projects. We hope to make some adjustments as soon as possible. Therefore, we have been calling for the establishment of the SIIP (Integrated Circuit Industry Technology Innovation Strategic Alliance) internationalization platform, hoping to become an international platform for capital flow and technology exchange, allowing Chinese capital to absorb more capital and experience, and international capital can find more Quality projects, this is the original intention of our support SEMI to do this forum.

The integrated circuit industry is a global industry, and with the transfer of the international semiconductor industry chain, the future Chinese IC market is the global market. However, due to the relatively weak domestic basic level, many of the current investment benefits are foreign equipment and materials companies. Next we are looking for a better cooperation model. A big trend in the future is a gesture of integration. It is not that Chinese companies acquire foreign companies and then convert them into domestic companies. Instead, Chinese companies go global and grow into international companies.

Q & A session:

1. At present, China often faces shortages of equipment and materials when establishing semiconductor production lines. What do you think of it?

Supply shortage is normal, especially in the current situation of large capacity expansion in China, and the future will enter the era of intelligence, not only in the consumer field, but also in the intelligent transformation of traditional industries. Big. For some operational actions carried out by foreign companies, we believe that this is a very short-sighted behavior, and it is also a good opportunity for domestic equipment and material supply chain.

2. What is the market share that China's current equipment and materials companies can share? Any suggestions for industrial development?

China's semiconductor equipment and materials products can supply no more than 10% (according to the amount), and overall it is still very weak, and foreign equipment and materials companies usually use some unfriendly dumping methods. In fact, I think this strategy is not Must be effective. In the long run, the market is growing at a rapid rate. For foreign-funded enterprises, it is better to let go of the development of Chinese companies than to stand up and develop with Chinese companies.

Chapter IV Regional Synergy, Building the Yangtze River Delta Integrated Circuit Core Heights

Shen Weiguo Chairman of China Integrated Circuit Industry Investment Fund, Managing Director of Shanghai Technology Venture Capital Group

Mr. Shen mainly discussed the opportunities, adjustments and suggestions for the development of the IC industry from the perspective of the Yangtze River Delta.

I. Development status of IC industry in the Yangtze River Delta

China's integrated circuit industry has formed four distinct industrial clusters. (1) Shanghai-centered Yangtze River Delta (2) Beijing-centered Bohai Bay (3) Shenzhen-centered Pan-Pearl River Delta (4) Midwest, represented by Wuhan, Xi'an and Chengdu

The Yangtze River Delta region, one city and three provinces, including Shanghai, Jiangsu, Zhejiang, and Anhui provinces, is China's IC industry with the most solid technology, the most complete industrial chain, and the most technologically advanced region. The industrial scale accounts for half of the country's total, design, manufacture, and testing. , equipment and materials are fully developed.

A group of international advanced enterprises, including Qualcomm, Dial-up, AMD, NVIDIA, MediaTek in the design industry; equipment giants AMAT, LAM, ASML, TEL, KT; wafer foundry TSMC, UMC, memory manufacturer Hynix, packaging and testing Leading ASE, such as ASE, set up R&D centers or branches in the Yangtze River Delta region.

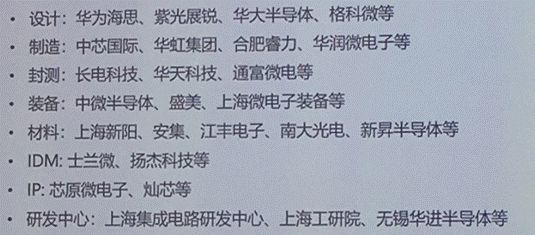

Local companies are also the first to gather together, which basically represents the most advanced productivity in the domestic segment, including Huawei Hisilicon in the design field, Ziguang Zhanrui, Huada Semiconductor, Gekewei, SMIC in the manufacturing field, Huahong Group, etc. , as well as packaging and testing, equipment, materials, IDM, IP and other fields.

2. Introduction to the development of each region by region

In 2017, the Shanghai IC industry achieved a “double harvest†in speed and quality.

The overall sales scale is close to 120 billion yuan, an increase of more than 12% year-on-year; the structure of the industrial chain is more optimized, and the situation of design, manufacturing, and equipment materials is basically formed. SMIC's 14nm technology development is progressing smoothly. The sales of Zhongwei Semiconductor has exceeded 1 billion. MOCVD has sold the world's top two, and the new silicon wafer has made breakthroughs. The test film has been supplied in batches;

Shanghai put forward the development goal of "secondary layout, secondary entrepreneurship, leading the industry to 200 billion mark", and will create three pillars of design, manufacturing and equipment materials by upgrading the industrial development strategy; expand the industrial development model and build IDM Mode of development, such as the third pole of the industry, to promote the development of the integrated circuit industry;

Established a total of 50 billion scale "1+1 +3" design mergers and acquisitions, equipment materials, manufacturing funds, invested in SMIC South 14nm, Huali integrated 28nm advanced technology production line and other major projects.

Jiangsu has always been an important base for the development of integrated circuits in China, and has gradually formed an integrated circuit industry belt along the Yangtze River centered on cities such as Wuxi, Suzhou and Nanjing.

In 2017, the sales volume reached 131.87 billion, a record high. During the 13th Five-Year Plan period, we strived to earn more than 300 billion yuan in the main business of the integrated circuit industry in the province.

Nanjing is accelerating the development of integrated circuits. The first phase of the $3 billion TSMC 12-inch wafer project is about to be mass-produced. The Tsinghua Unisplendour project with a total investment of 80 billion yuan has started construction. A number of supporting enterprises such as the US Air Chemical Industry have successively entered the world. The first two EDA suppliers Synopsys and Cadence settled in Nanjing, and the industry chain continued to improve.

In 2017, Wuxi City's IC production value reached 89 billion, mainly including Hynix DRAM manufacturing base, China Resources Microelectronics and so on. Huahong Wuxi IC R&D and manufacturing base project has started construction, and Hynix's 100-inch wafer foundry production line with 100,000-piece capacity will also be moved in.

Anhui Province proposed the "Shuxin Plan" to accelerate the scale and level of the integrated circuit industry.

Anhui is a rising star in the development of integrated circuits. As the core city of Anhui's development of semiconductor industry, Hefei has initially formed a relatively complete semiconductor industry chain, with more than 100 integrated circuit companies, including 12-inch production lines such as Rui!

By 2020, we will build 3-5 8-inch or 12-inch wafer production lines with a combined production capacity of over 100,000 to 150,000 pieces per month. We will cultivate and introduce more than 30 design companies to form IDM companies in several specific industries. The industry entered the top five in China, and the manufacturing industry ranked in the top three in the country;

The industrial sales revenue has reached 500-100 billion yuan, making it the largest production base for specific chips such as panel drivers, automotive electronics, power integrated circuits, and specialty memories.

Zhejiang also entered the fast lane of integrated circuit development.

Hangzhou has promulgated an integrated circuit industry development plan with the goal of achieving an industry scale of 50 billion by 2020.

Silan Micro and the Big Fund jointly built an 8-inch production line in Hangzhou and a 12-inch production line with Xiamen. Ningbo and Shaoxing jointly established an 8-inch production line with SMIC.

Alibaba is crazy about investing in artificial intelligence and IoT chip design companies, and a number of outstanding terminal companies represented by Hikvision and Dahua shares bring huge opportunities for local chips.

The linkage of the industrial chain in the Yangtze River Delta region has gradually started and achieved a good start.

SMIC participates in Changjiang Electronics Technology Co., Ltd. to deepen the business cooperation between wafer fabrication and packaging and testing, and provide customers with better solutions!·Huahong Group and Wuxi local government cooperate to invest 10 billion US dollars to build several 12-inch production lines. Became the fourth manufacturing base of Huahong Group following Jinqiao, Zhangjiang and Kangqiao;

SMIC cooperates with Zhejiang Ningbo and Shaoxing to build an 8-inch specialty fab to meet the growing market demand; Huada Semiconductor participates in Shanghai Advanced Semiconductor, from design extension to manufacturing, aiming to create a market-oriented and automotive electronics market. Analog and power device IDM companies;

Hikvision's investment in Fuwei is the vertical cooperation between the terminal and the chip. Fuyu has the opportunity to rely on Haikang's large platform to usher in the great development of the business.

Guangzhou Yunge Tianhong Electronic Technology Co., Ltd , https://www.e-cigarettesfactory.com